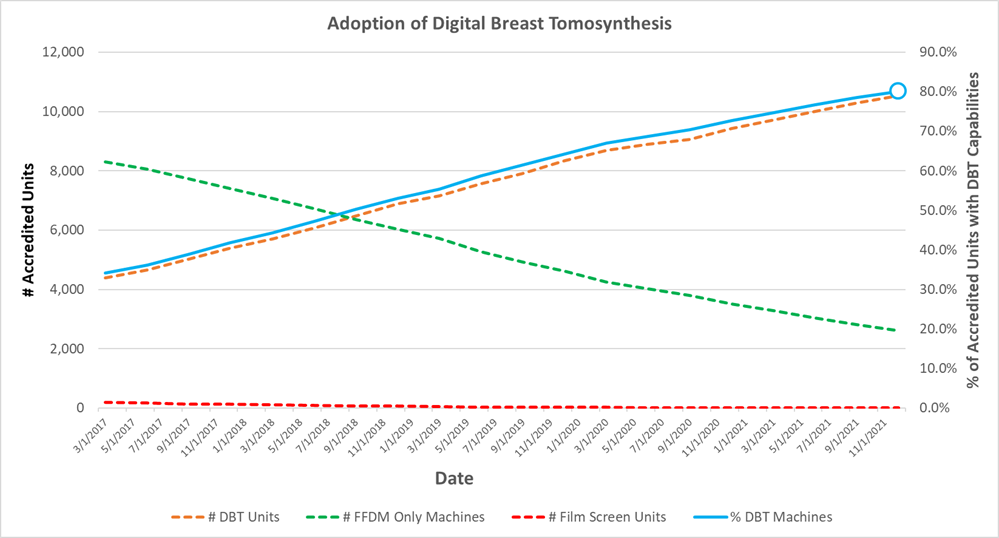

On the heels of a very successful RSNA 2021, a major milestone has been reached. For the first time, the number of tomosynthesis-capable mammography systems in the United States exceeds 80% of the installed base. In the latest MQSA statistics, the FDA reported that of 13,147 distinct X-ray units, 10,537 (80.1%) are tomosynthesis-capable.

This milestone is important because I think it clearly puts us into the “tomosynthesis as the standard of care” arena. But the MQSA data does not do several other things:

- It does not tell us how many screening mammograms are performed with tomosynthesis

- It does not tell us the typical triage to 3D or 2D that is used across the United States, and

- It does not tell us how tomosynthesis is applied in cases of repeat images or mosaic images where total dose might be a concern.

FDA began reporting DBT accreditation data in June 2016. Between that time and now, the growth of DBT has been both remarkable and remarkably linear. While in June 2016 there were 3,362 machines installed (26.3%) of 12,793 distinct gantries, today the market penetration exceeds 80%.

It is not clear why the growth appears so linear, which isn’t what you expect in a market that is “taking off”. Perhaps it is because sites have struggled with the reading times, the amount of data, or the cost of the equipment. But the march of DBT in the US has been relentless, not even slowing down for COVID-19.